‘Participating’ vs ‘Non-Participating’ Plan in Life Insurance

-

Customer Service

-

Our Products

- Edelweiss Life - Assured Income STAR - A Regular Guaranteed¹ Income Plan

New Launch

- Edelweiss Life - Guaranteed Flexi STAR - Assured¹ Savings Plan

- Edelweiss Life – Wealth Rise+ - A Double - Advantage ULIP

- Edelweiss Life – Wealth Plus - A Savings, Insurance & Child Benefit Plan

- Edelweiss Life - Zindagi Protect Plus - A Comprehensive Term Plan

New Term Plan

- Edelweiss Life - Premier Guaranteed Star

- All Products

- Edelweiss Life - Assured Income STAR - A Regular Guaranteed¹ Income Plan

-

Resume Application

-

Insurance Guide

-

Knowledge Center

- Savings Plans

- Life Insurance

- Term Insurance plans

- Unit Linked Insurance Plans

- Guaranteed Income Plans

- Retirement Insurance

- Health Insurance Plans

- Child plans

- Insurance Fraud Awareness

- Covid Insurance

- NRI Insurance

- Investment Plans

- Endowment Plans

- Group Insurance

- Micro Insurance

- Sabse Pehle Life Insurance

‘Participating’ vs ‘Non-Participating’ Plan in Life Insurance

6/13/25 10:30 AM

Blog Title

16603 |

6/13/25 10:30 AM |

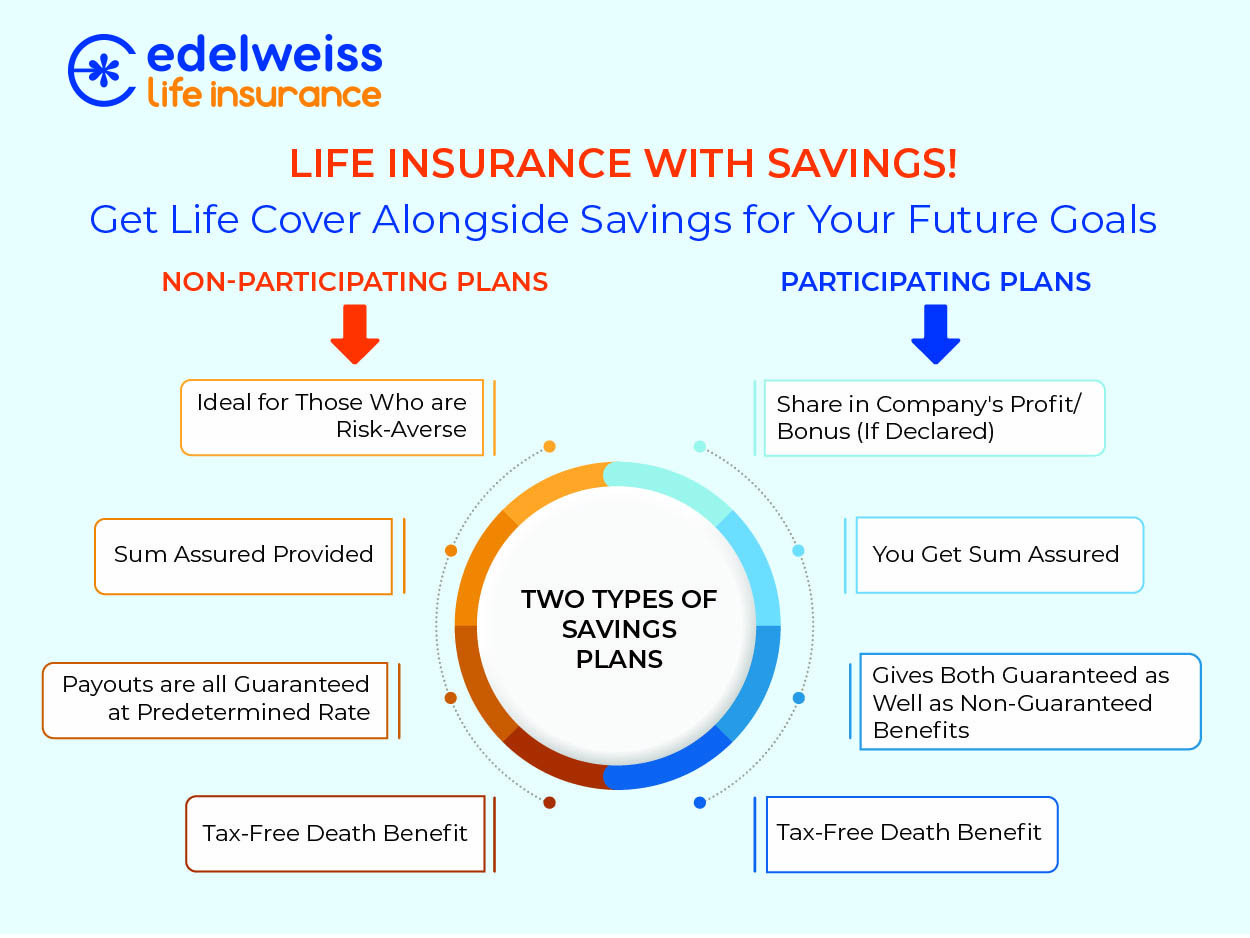

Life insurance plans that also offer a savings element generally come under two categories, ‘Participating’ and ‘Non-Participating’ or ‘Par’ and ‘Non-Par’. You might be interested in buying a savings insurance plan and may have come across these terms while comparing various plans.

To put it simply, a ‘participating’ plan is one where a part of your premium is invested into the insurance company itself. On the other hand, a ‘non-participating' plan lacks this investment element and generally offers completely guaranteed returns.

Read on to learn more about the nuances of a participating insurance plan and how it can help you grow your wealth.

First Understand the Difference between Guaranteed and Non-Guaranteed Returns

Most savings insurance plans are ‘guaranteed returns’ plans, meaning that you know exactly how much money you will get back as a return on your investment. These plans are ideal for those who are risk averse and want an investment with assured growth. A plan that purely offers guaranteed returns will always be a non-participating plan.

If an insurance plan is tagged as ‘participating’, then there will also be a non-guaranteed element to it. ‘Non-guaranteed’ returns basically means that you do not know the exact growth rate for your investments and cannot accurately predict how much money you will get back. Participating plans generally include a certain element of risk, as the non-guaranteed returns will depend on the performance of the insurance company. The better the company performs; the better will be your returns. Generally, non-guaranteed returns of a participating plan are provided in the form of a ‘cash bonus’.

Example of Participating Life Insurance Policies

A great example of a participating plan is Edelweiss Life- Flexi Savings Plan. When you purchase a participating or ‘par’ plan like Flexi Savings Plan, you invest a part of your premiums into the insurance company. This makes you eligible for profit-sharing benefits. Every financial year, when an insurance company discloses their profits, you will receive a segment of those profits in the form of a cash bonus. This cash bonus can either be received as income, or it can be added onto the sum assured received on death, or it can be paid out at the very end of your policy term as a maturity benefit.

Features of a Participating Plan

Participating plans always have a ‘cash value’ that grows over time.

Participating plans offer returns in the form of a ‘bonus’. This bonus can be paid our regularly (called cash bonus), or it can accrue over time and be paid out at maturity (revisionary bonus).

The bonus rate for a participating plan is declared each year. This declared rate will depend on the insurance company’s financial performance and is a form of ‘profit sharing’.

All par plans come with a life cover element to secure your family in case of your death. A ‘terminal bonus’ is also applied to your life cover amount and is payable alongside your total death benefit.

Benefits of a Participating Plan

The cash bonus received from a participating plan can be a great source of secondary income.

Bonuses received via participating plans can often exceed the guaranteed returns if the insurance company is performing well.

You can choose to reinvest the cash bonus with the insurer to further enhance your returns.

Some policies allow you to pay off your year’s premium using the cash bonus itself, meaning that your policy can pay for itself once it starts accruing profits.

Participating Plans: Who is it for?

Participating plans are ideal for those who want a long-term savings insurance plan that offers decent returns at moderate risk. Since bonus declarations are non-guaranteed, there is a chance of getting lower returns than expected if the insurance provider underperforms. However, a well-performing insurance company generally offers bonus rates that are greater than most guaranteed savings plans. So, par plans tend to consistently provide better returns except in cases of poor company performance.

Of course, par plans also offer life cover to secure your loved ones in your absence. Bonuses also apply to your death benefit, which can further enhance your family’s financial security in case of your untimely death.

Example of Non-Participating Life Insurance Policies

Non-participating life insurance plans, better known as guaranteed income life insurance plans, are savings oriented financial products that offer a set rate of returns for the entire policy term. A classic example of a guaranteed savings plan is Edelweiss Life- Guaranteed Savings STAR. In this plan, you get completely guaranteed returns at maturity. The rate of returns for your plan is set at the inception of your policy and remains the same until the end of your policy term. Guaranteed savings plans allow you to calculate your future returns on day one itself, which in turn, allows you to create an accurate financial plan for your life goals.

Features of Non-Participating Plans

Rate of Returns are guaranteed.

Plans have a cash value/surrender value that grows over time.

You can get guaranteed income or choose to wait until maturity to get lumpsum payout.

Life cover is provided to secure your family.

Benefits of Non-Participating Plans

Since returns are guaranteed, you can accurately make a financial plan for your future goals.

Non-participating plans are low-risk investments as your rate of returns are completely static, protecting you from the volatility of market instability.

Some guaranteed plans offer regular income that can further boost your monthly expenditure.

Guaranteed savings life insurance plans also help you secure your dependents via the life cover element.

Non-Participating Plans: Who is it for?

Non-par/guaranteed plans are ideal for those who want to grow their savings without dealing with the risk of unsteady returns. Since the return rates are guaranteed, you do not have to worry about market downturns or your insurance providers poor financial performance. You know exactly what you are going to get back from day one of your policy. Those who are risk averse or want a steady income source to support their loved ones will prefer to invest in a non-par plan.

Key Differences Between Participating and Non-Participating Plan

|

Participating Plan |

Non-Participating Plan |

Profit-Sharing |

Has profit-sharing element as returns are directly linked to insurance company’s performance. |

No profit-sharing element. All returns are guaranteed at the start of the policy. |

Risk |

Slight risk due to returns being linked to company’s profits. If the insurer performs poorly, then returns will also be lower. |

Low risk. As returns are guaranteed, you can expect the same returns irrespective of company performance. |

Rate of Returns |

Potential for higher returns if the insurance company’s profits are high. |

Rate of returns are set at the start of the policy and never change; hence, the growth rate is generally modest. |

Ideal For |

Customers who are risk savvy and looking for higher returns. |

Customers who are risk averse and want returns that are completely guaranteed. |

Are ULIPs Classified as Participating Plans?

Unit Linked Insurance Plans (ULIPs) are a unique type of insurance where a part of your premium is invested into market linked funds. This means that your returns are not based on the company’s performance, but rather the performance of the market funds that you’re invested into. Of course, a ULIP can also be a participating plan if the insurer offers profit-sharing benefits as part of the policy terms.

But in general, ULIPs and participating plans are considered to be different insurance products based on the nature of investment. However, both types of insurance are non-guaranteed.

A Chance of Better Returns!

The main advantage of buying a participating plan is the chance of getting a higher return on investment compared to a guaranteed plan. If you are willing to take on a bit of risk and trust the insurer you are investing in, then participating plans are the way to go.

FAQs

What is PAR and non-PAR in life insurance?

PAR refers to participating plans where your returns will depend on the financial performance of your life insurance provider. Non-PAR refers to non-participating plans (guaranteed returns/endowment plans) where your returns are completely guaranteed, and your interest rates remain the same throughout the policy term.

Are participating policies more expensive than non-participating policies?

Generally, participating plans are slightly more expensive than non-participating plans, as you will receive a part of your insurance company’s profits as returns. However, participating plans also tend to offer greater returns when compared to non-participating plans, especially if your insurance company is doing well financially. The cost of your plans can also differ based on the insurance provider of your choice, your plan’s specific terms and conditions, and the prospective returns you want from your plan.

Can the dividends in a participating policy fluctuate?

Yes, participating plans are non-guaranteed, meaning that you rate of returns can differ from year to year. The returns you get from a participating plan depends on your insurance provider’s annual profits. So, a good financial year can lead to higher returns while a poor financial year can lead to lower returns.

Are there tax implications for dividends received in a participating policy?

Yes, income/returns received from a participating policy may be subject to taxation. However, if you plan meets the terms and conditions of Section 10(10D) of the Income Tax Act, 2025, then you can opt for complete tax exemptions for your returns.

How do I know if a policy is participating or non-participating?

Participating plans pay returns in the form of ‘bonuses’. So, any plan that includes the words cash bonus, revisionary bonus, or terminal bonus, will be participating plans. On the other hand, non-par plans are generally guaranteed, and the word ‘guaranteed returns/income’ will be highlighted in the brochure.

Aastha Mestry - Portfolio Manager

An Author and a Full-Time Portfolio Manager, Aastha has 6 years of experience working in the Insurance Industry with businesses globally. With a profound interest in traveling, Aastha also loves to blog in her free time.

Related Blogs