5 Simple Tips to Save Your Money & Secure Your Finances

-

Customer Service

-

Our Products

- Edelweiss Life - Assured Income STAR - A Regular Guaranteed¹ Income Plan

New Launch

- Edelweiss Life - Guaranteed Flexi STAR - Assured¹ Savings Plan

- Edelweiss Life – Wealth Rise+ - A Double - Advantage ULIP

- Edelweiss Life – Wealth Plus - A Savings, Insurance & Child Benefit Plan

- Edelweiss Life - Zindagi Protect Plus - A Comprehensive Term Plan

New Term Plan

- Edelweiss Life - Premier Guaranteed Star

- All Products

- Edelweiss Life - Assured Income STAR - A Regular Guaranteed¹ Income Plan

-

Resume Application

-

Insurance Guide

-

Knowledge Center

- Savings Plans

- Life Insurance

- Term Insurance plans

- Unit Linked Insurance Plans

- Guaranteed Income Plans

- Retirement Insurance

- Health Insurance Plans

- Child plans

- Insurance Fraud Awareness

- Covid Insurance

- NRI Insurance

- Investment Plans

- Endowment Plans

- Group Insurance

- Micro Insurance

- Sabse Pehle Life Insurance

5 Essential Money-Saving Tips for Young Adults

6/26/24 4:30 AM

Blog Title

6667 |

6/26/24 4:30 AM |

Saving money is the first thing every young adult should learn once they start earning. However, it doesn’t come naturally to most of us. As per a report published by CEIC, India Gross Savings Rate was measured at 30.2% in Mar 2023, compared with 31.2% in the previous year. The data was at an all-time high of 30.2% in Mar 2008.

Everyone knows the importance of saving money. All of us have dreams for the future that can only be fulfilled with a proper financial plan. For example, buying a house is a common aspiration for many young people, but amassing the wealth required for such a purchase is not easy. Let’s take a look at 5 simple tips that you can follow to save money and secure your finances, one step at a time.

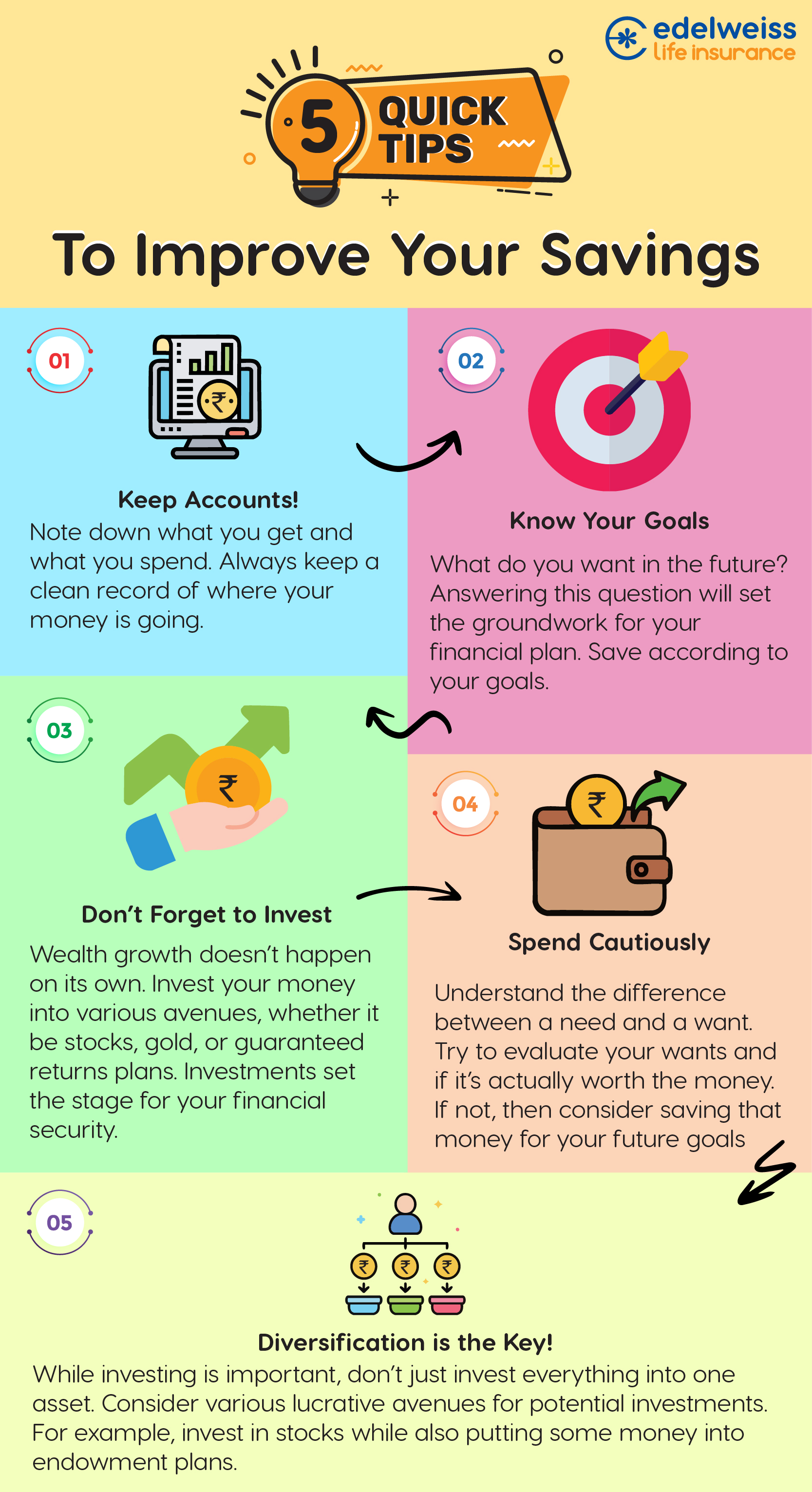

1. Keep Accounts.

Always have a clear account of where your money is going! Whether you have money saved in a bank, have various investments, or are paying monthly premiums for an insurance plan, always keep an account of your finances. Tracking your income and expenditures will help you sustain your wealth growth. You will also be able to quickly cut off investments that are performing poorly before you lose too much money.

2. Set Your Financial Goals.

One of the first things you need to do is set financial goals for yourself. Want to save money for a new laptop, for your marriage, or for your child’s education? All of these are life goals that can only be fulfilled by saving appropriately. Divide your goals based on how much time you have to fulfil them. Some goals, such as savings for a vacation, are short-term. On the other hand, saving for your child’s education is a long-term goal that necessitates long-term planning. Ensure that you allot proper time limits to each goal and try your best to meet those financial goals within the planned period.

3. Investments are a Must!

Always invest a part of your savings into various assets that grow in value. Keeping your money saved in a bank account is fine, but that does not assure the growth of your wealth. Remember that the value of money goes down over time! Inflation is a constant issue that increases the cost of living. The value of a ₹100 note today is not the same as it was two decades ago, simply because things have become much more expensive. So, invest your money into things that have the potential to grow in value! You can invest in stocks, gold, real estate, or other funds that grow over time.

Unit-Linked Insurance Plans (ULIPs) are a popular investment option that also provides life cover for your family in case of your unfortunately demise. In a ULIP, your premiums are invested into various market-linked funds that grow in value according to the current market rates. ULIPs offer a diverse range of funds that suit different types of investors. For example, if you want high returns and are willing to take risks, then choose equity funds. But if you want steady returns and are risk averse, then you can invest into ULIP debt funds instead.

However, if you prefer completely assured returns, then opt for a guaranteed income plan. Guaranteed income plans provide returns at a set rate of interest that never changes! So, you know exactly how much money you are getting back as a return on your investment. Guaranteed income plans are ideal for those who are risk-averse or want steady income during their retirement.

4. Spending Money Cautiously.

Spending your earning on some new gadget may sound alluring but ask yourself if buying that gadget is necessary. Will it create a hole in your pocket that will be difficult to patch? And can you afford to survive without that money in case of an unforeseen emergency? Buying something on a whim might sound fine right now, but it may cause unexpected financial problems in the future. If you just ‘want’ to buy something without cause, then reconsider. Exercise caution before making any purchase. Don’t pursue short-term wants at the cost of your long-term goals.

5. Pick the Right Tools & Diversify.

Don’t keep all your eggs in one basket! This is especially true when it comes to investments. While investing is important to grow your savings, avoid putting all your money into one asset. Even if your investment seems great, the risk of losing everything if that one investment fails is just too high. Invest parts of your savings in different assets that complement one another. For example, if you’re investing in stocks, then also consider investing in a guaranteed income plan to compensates for the volatility of the share market.

Learn to Save; Learn to Thrive!

Ensure that you are always setting aside a part of your income as savings. Think of saving money as a good habit that you need to cultivate for a secure and healthy future. In fact, you should try to save at least 30% of your annual income as a general practice.

Moreover, alongside all the tips given above, try to maintain an emergency fund that you can use during an unexpected crisis. This emergency fund will help you avert financial problems without having to dip into your investments. You can also invest in a guaranteed income plan if you want to create a source of passive income for your family. This passive income can not only help during emergencies but can also help you fulfil your financial goals.

Most importantly, try to grow your wealth to fulfil your dreams! If you are regular with your savings, maintain your accounts, and avoid irresponsible expenditures, then you will surely amass enough wealth to fulfil your goals.

Aastha Mestry - Portfolio Manager

An Author and a Full-Time Portfolio Manager, Aastha has 6 years of experience working in the Insurance Industry with businesses globally. With a profound interest in traveling, Aastha also loves to blog in her free time.

Related Blogs